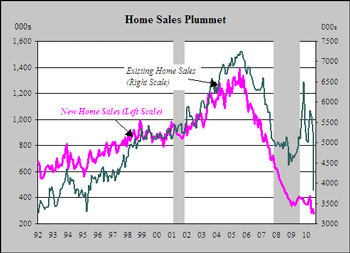

Depending on your location, home sales experienced a rise or a fall in August. Within the US, California saw an all-time low while British Columbia, Canada, had a temporary increase in home sales. California experienced a drop in many areas of real estate.

California, US – Fall in Home Sales

Home sales in California fell 2.7% from July. That drop in one month seems small compared to other statistics. Home sales fell 20% from June-July 2010 and 14% from August 2009. As well, the median price ($260,000) of California homes dropped 3% in August from July.

San Francisco Bay Area

Within the San Francisco Bay area, the median home price was $385,000. This figure is a 4.2% drop from the median price in July ($402,000). Home sales fell 1.1% in August from July and 10.9% from August 2009. 6,698 homes were sold last month compared to 7,518 homes in the previous August. This drop puts home sales in the Bay area at their lowest point for the month in eighteen years.

Some potential buyers are waiting for prices to fall further and other people are just waiting to be in a position to buy a home. Despite falling prices and low mortgage rates, joblessness is one factor that is having a huge effect on home sales. As well, first-time home buyers no longer have the Home Buyers' Tax Credit to ease the burden.

Foreclosures

While everything else was falling during August in California, foreclosures increased over July's rate. Foreclosures rose from 35.9% to 35.2%. In the San Francisco Bay area, foreclosures accounted for 26.7% of resales in August compared to 25.3% in July. Foreclosures are, however, down from last year during August – down 42.8% on average in California and 24.8% in the San Francisco Bay area.

British Columbia, Canada – Rise in Home Sales

Home sales rose (4.1%) in Canada during August compared to the previous month's purchases. July records indicated that it took 7.3 months to sell a home in Canada. August records point to a 6.9 month wait. Yet experts in Canadian real estate do not expect a continued rise throughout the rest of the year.

"Rising interest rates and a projected slowdown in job growth mean that the Canadian housing market is expected to continue to cool," said Georges Pahud, president of CREA.

Although August statistics might be better, sales in July were not high despite the fact that June saw considerable sales. Most buyers in June, however, were trying to purchase before the new HST (Harmonized Sales Tax) regulations came into effect in July.

August sales are probably a throwback to the incredible rate of sales in 2009. During that year, home sales rose by 66% and prices increased by almost 22%. It is hard for any system to maintain that level of activity so things have leveled off somewhat in 2010.

"I don't see the continuation of a dizzying descent in sales activity," says REA chief economist Gregory Klump.

Some changes in Canadian real estate are just marginal improvements. The average price of a Canadian home during August was $324,928. In 2009, the price came in at $324, 843. Demand has increased (1.9%) since last summer but dropped 16% from the peak in April. The Canadian Real Estate Assocaition (CREA) expects home prices to fall but not at any substantial rate.

Are Home Sales Rising Or Falling In Your Area?

Image courtesy of jpturnercompany.blogspot.com